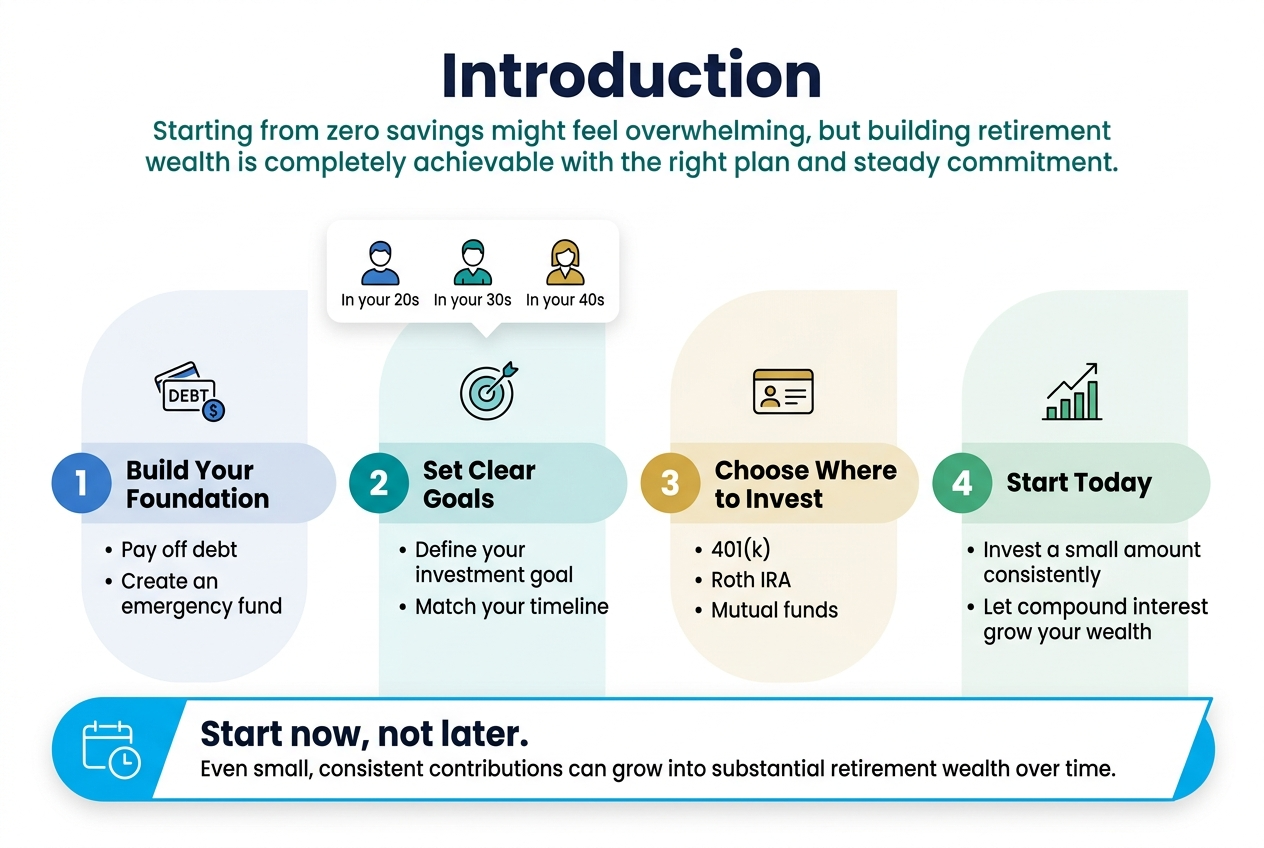

Starting from zero savings might feel overwhelming, but building retirement wealth is completely achievable with the right plan and steady commitment.

This guide is for anyone who’s ready to take control of their financial future but doesn’t know where to begin. You might be in your twenties just starting your career, in your thirties realizing you need to get serious about retirement, or even in your forties feeling behind but determined to catch up.

You’ll learn how to build your financial foundation before investing, including paying off debt and establishing an emergency fund. We’ll walk through setting clear investment goals and determining exactly how much to invest based on your income and timeline. Finally, you’ll discover how to choose the right investment accounts and types for long-term growth, from 401(k)s to Roth IRAs to mutual funds.

The key is starting today, not waiting for the “perfect” time or a larger paycheck. Even small, consistent contributions can grow into substantial retirement wealth thanks to compound interest working in your favor over time.

Build Your Financial Foundation Before Investing

Pay Off All Consumer Debt Using the Debt Snowball Method

The debt snowball method provides a systematic approach to eliminating consumer debt by focusing on paying off smallest balances first while maintaining minimum payments on larger debts. This strategy builds psychological momentum as you witness quick wins, creating motivation to tackle larger debts systematically.

Save $1,000 Starter Emergency Fund

Before investing in retirement accounts, establish a $1,000 starter emergency fund to cover minor unexpected expenses. Research shows that 37% of adults would struggle to cover an unexpected $400 expense, highlighting the critical importance of having immediate access to emergency funds for basic financial stability and peace of mind.

Set Clear Investment Goals and Determine How Much to Invest

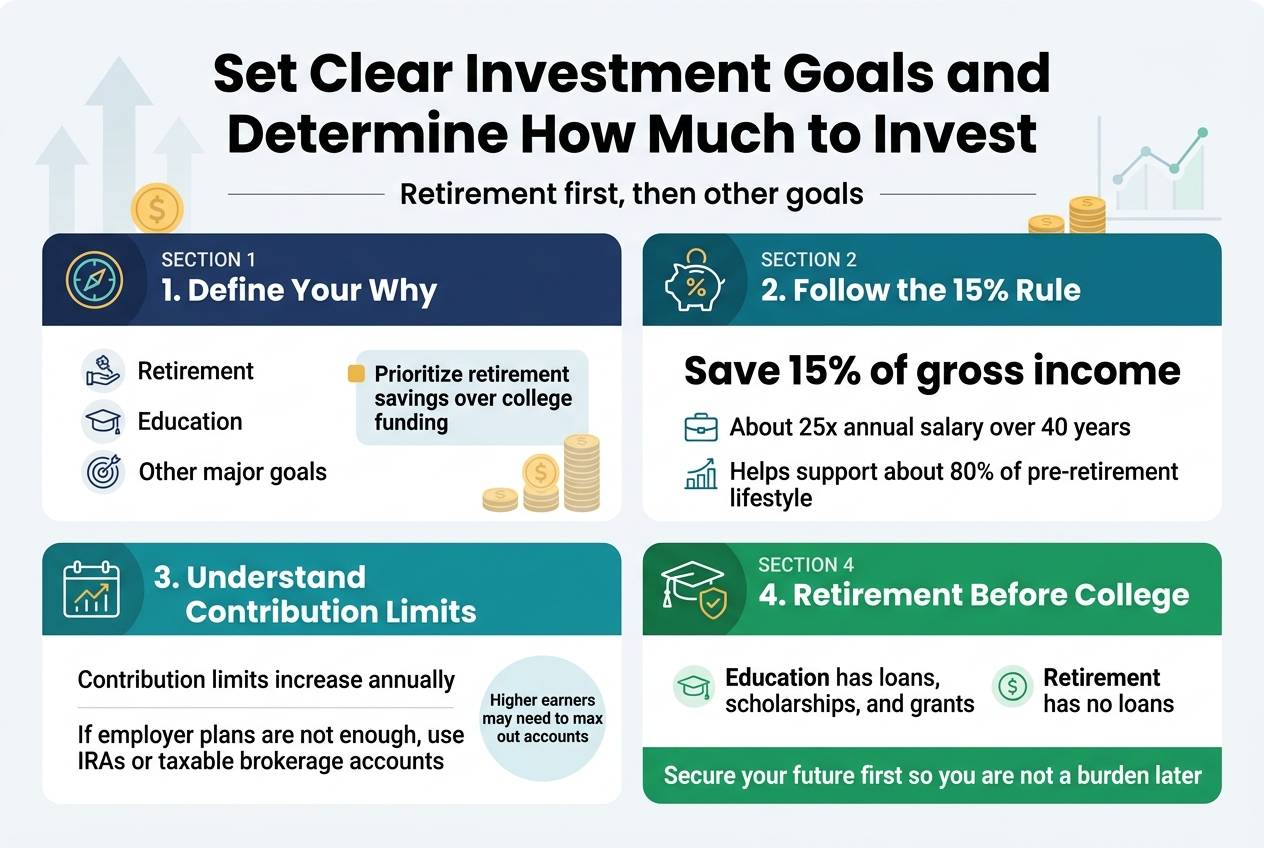

Define Your Why: Retirement, Education, or Other Goals

Before diving into specific contribution amounts, it’s crucial to clarify your investment objectives. While retirement should be your primary focus, you may also consider other goals like education funding or major purchases. However, financial experts consistently recommend prioritizing retirement savings over children’s college expenses, as there are loans available for education but no loans for retirement.

Follow the 15% Rule for Retirement Savings

The 15% rule serves as the foundation for retirement planning, representing the minimum percentage of your gross income you should save annually throughout your career. This guideline, developed through extensive research by economists and investment companies, is designed to help you accumulate approximately 25 times your annual salary over a 40-year career. When combined with Social Security benefits, this savings rate should enable you to maintain roughly 80% of your pre-retirement lifestyle.

Understand 2026 Contribution Limits for Retirement Accounts

While the reference content doesn’t specify exact 2026 limits, it’s important to understand that contribution limits increase annually. For higher earners making around $153,000 or more, maxing out retirement account contributions becomes essential to reach the 15% savings target. If you can’t contribute the full 15% through employer plans alone due to contribution limits, you’ll need to supplement with additional investment accounts like IRAs or taxable brokerage accounts.

Prioritize Retirement Over Children’s College Savings

Financial planning experts universally recommend prioritizing your retirement savings over funding your children’s college education. This strategy makes practical sense: students can access loans, scholarships, and grants for education expenses, but no such options exist for retirement funding. Additionally, by securing your own financial future first, you avoid becoming a financial burden on your children later in life, ultimately serving both your interests and theirs.

Choose the Right Investment Accounts for Your Goals

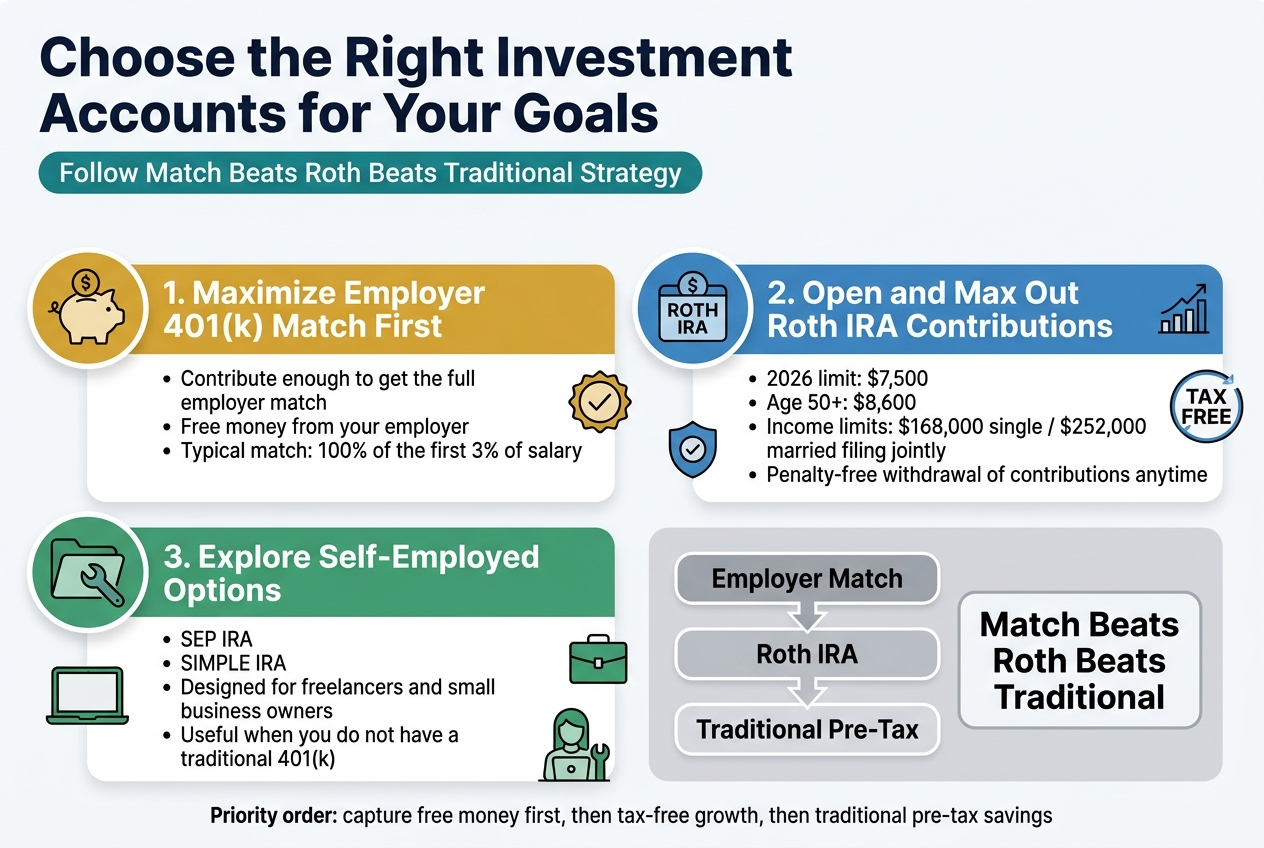

Follow Match Beats Roth Beats Traditional Strategy

When building retirement wealth from zero, understanding the priority order for contributions is crucial. The “Match Beats Roth Beats Traditional” strategy provides a clear roadmap: first maximize employer matching contributions, then focus on Roth accounts, and finally consider traditional pre-tax accounts. This approach ensures you capture free money from employer matches while prioritizing tax-free growth potential in retirement through Roth contributions.

Maximize Employer 401(k) Match First

Previously, we’ve established your financial foundation, so now it’s time to prioritize the most valuable retirement benefit available. If your employer offers a 401(k) match, contribute enough to receive the full matching contribution before investing elsewhere. This employer match represents free money—typically 100% of the first 3% of your salary—that you’d be leaving on the table otherwise. Even if you can only afford small contributions initially, securing this match should be your absolute priority.

Open and Max Out Roth IRA Contributions

With your employer match secured, the next step involves opening a Roth IRA for maximum flexibility and tax advantages. For 2026, you can contribute up to $7,500 annually ($8,600 if you’re 50 or older) to a Roth IRA, provided your modified adjusted gross income stays below $168,000 for single filers or $252,000 for married couples filing jointly. Roth IRAs offer superior investment options compared to most 401(k) plans and allow penalty-free withdrawal of contributions at any time, making them ideal for beginners building wealth.

Explore Self-Employed Options: SIMPLE IRA and SEP IRA

Self-employed individuals and independent contractors have access to specialized retirement accounts beyond traditional options. SEP IRAs and SIMPLE IRAs offer different tax benefits, qualification requirements, and contribution methods designed specifically for small business owners and freelancers. These work-related alternatives provide similar tax advantages to employer-sponsored plans while accommodating the unique needs of self-employed workers who lack access to traditional 401(k) benefits.

Select the Best Investment Types for Long-Term Growth

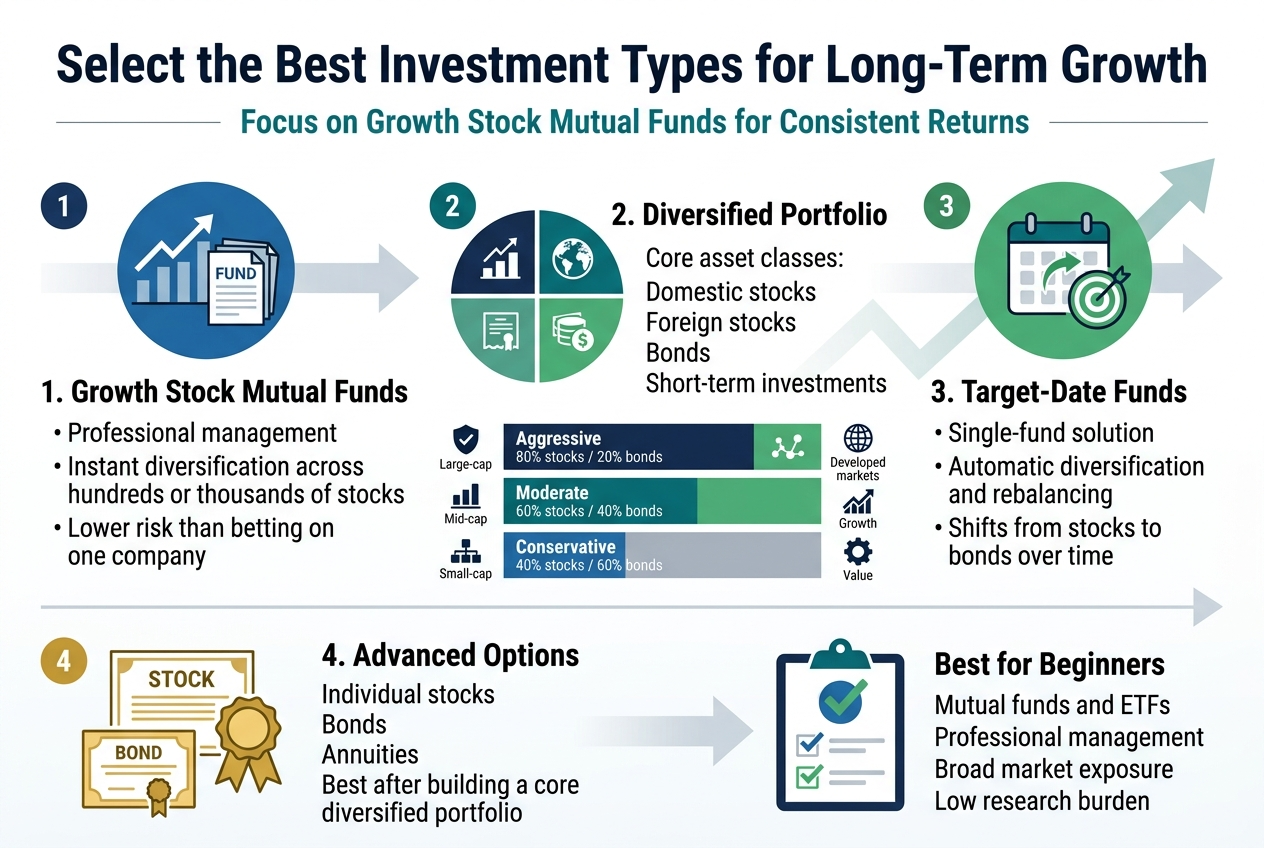

Focus on Growth Stock Mutual Funds for Consistent Returns

Growth mutual funds serve as the cornerstone of long-term retirement wealth building. These professionally managed collections of stocks provide instant diversification across hundreds or thousands of securities, eliminating the need to research individual companies while reducing the risk of investing everything in a company that goes under.

Build a Diversified Portfolio with Four Fund Types

Now that we understand growth funds, building a well-diversified portfolio requires spreading investments across four core asset classes: domestic stocks, foreign stocks, bonds, and short-term investments. Asset allocation strategies vary based on risk tolerance, with aggressive portfolios typically holding 80% stocks and 20% bonds, moderate portfolios maintaining 60% stocks and 40% bonds, and conservative approaches favoring 40% stocks and 60% bonds. Within each asset class, diversification extends to market capitalization (large-, mid-, and small-cap companies), various sectors like technology and healthcare, geographic regions including both developed and emerging markets, and different investment styles balancing growth and value stocks.

Understand Target-Date Funds for Low-Maintenance Investing

Previously, I’ve discussed building custom portfolios, but target-date funds offer a single-fund solution that automatically manages diversification and rebalancing. These funds adjust asset allocation over time, gradually shifting from higher-risk stocks to more conservative bonds as retirement approaches, eliminating the need for manual portfolio maintenance.

Consider Individual Stocks, Bonds, and Annuities for Advanced Strategies

With this foundation in mind, advanced investors may explore individual securities once they’ve established their core diversified portfolio. However, mutual funds and ETFs remain the most efficient path for beginners, providing professional management and broad market exposure without requiring extensive research or large capital requirements.

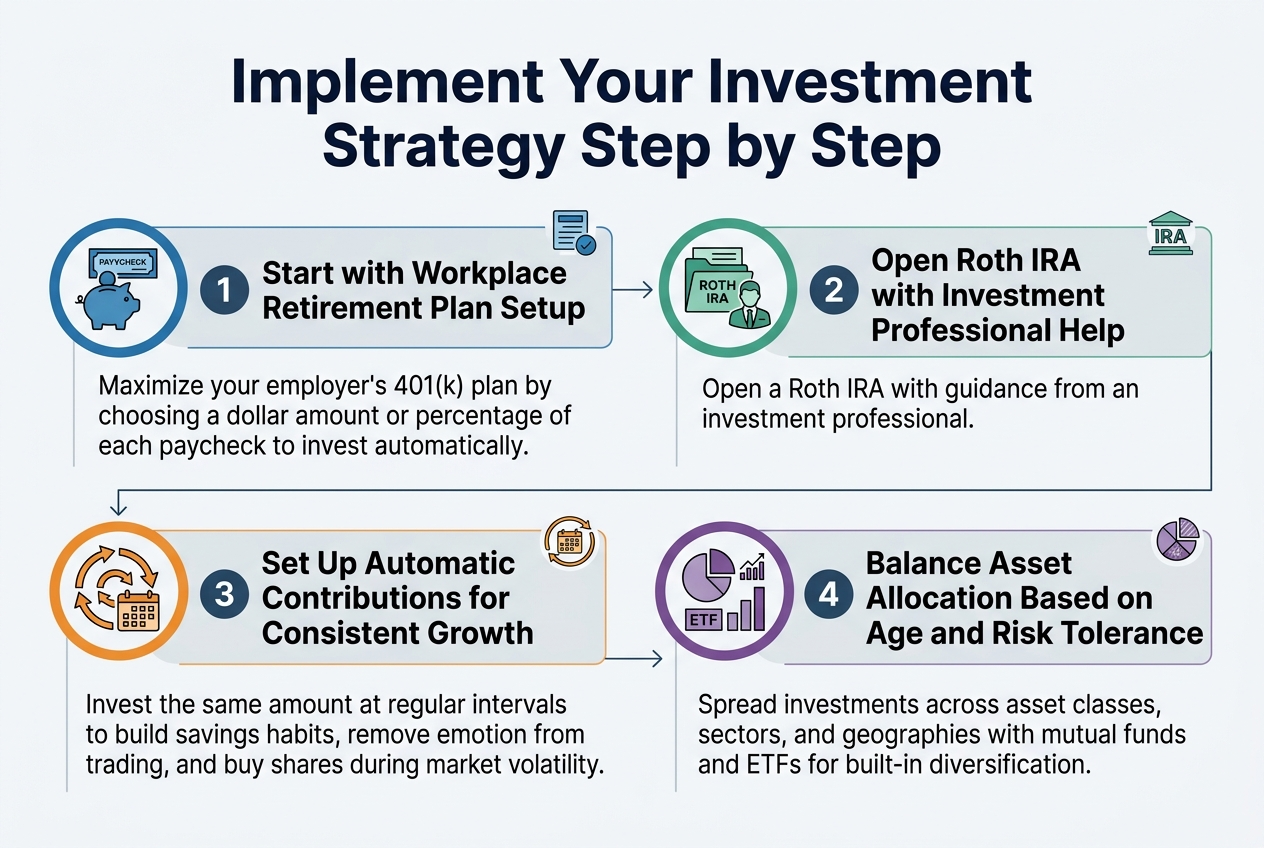

Implement Your Investment Strategy Step by Step

Start with Workplace Retirement Plan Setup

Now that you’ve determined your investment goals and selected appropriate accounts, the first practical step is setting up your workplace retirement plan. Most companies allow you to choose either a dollar amount or percentage of each paycheck to automatically invest in your employer-sponsored retirement plan. This systematic approach ensures you’re investing consistently without having to make repeated decisions about contributions.

Setting up your 401(k) contributions creates an automated foundation for your retirement savings strategy. By establishing this recurring investment plan through payroll deduction, you’re prioritizing your financial future by investing in yourself first. This process removes the stress and hassle of making manual contributions while helping you form positive investing habits that build wealth over time.

Open Roth IRA with Investment Professional Help

With your workplace plan established, the next step involves opening a Roth IRA to maximize your tax-advantaged growth opportunities. Working with investment professionals during this setup process ensures you understand the eligibility requirements and contribution limits that apply to retirement accounts like IRAs.

When establishing recurring investing for your IRA, you can choose the maximum contribution limit, which helps ensure you’re maximizing these valuable tax-advantaged growth opportunities. Investment professionals can guide you through creating an investment account, linking your funding account, and selecting appropriate investments that align with your time horizon, risk tolerance, and financial goals.

Set Up Automatic Contributions for Consistent Growth

Previously, we’ve established the foundation with workplace plans and IRAs. Now, implementing automatic contributions becomes crucial for consistent portfolio growth. Recurring investments allow you to establish repeat investments with the same amount of money at regular intervals, helping you develop disciplined savings habits and make measurable progress toward your investment goals.

This automatic investing process, also known as recurring investments, offers several significant benefits. It reduces the stress and hassle of making regular manual contributions since you won’t have to worry about remembering to contribute to your investment accounts. The system ensures consistent scheduling and helps you form positive investing habits by minimizing the need for repeated decision-making.

Setting up recurring investments is straightforward: choose your investment amount, select your frequency (weekly, every 2 weeks, or monthly), and create your schedule by choosing when you’d like contributions to begin. You can link your bank account to fund investments automatically, or use your existing account balance. The flexibility allows you to adjust or stop recurring investments at any time as your financial situation changes.

By investing consistently through automatic contributions, you’re putting good financial habits into action. This disciplined approach helps take emotion out of investment decisions while spreading your investment purchases over time, which can help reduce the risk of buying investments when prices might be relatively high or volatile.

Balance Asset Allocation Based on Age and Risk Tolerance

With automatic contributions flowing consistently, balancing your asset allocation becomes essential for long-term success. You should select your investments based on your financial goals, time horizon, and risk tolerance. Taking an investor questionnaire can help you decide how to allocate investments among different asset classes, including stocks, bonds, and short-term reserves.

Building a diversified portfolio involves spreading investments across different asset classes, sectors, and geographies while using different investment styles. Diversification helps reduce overall investment risk because when you spread money across multiple investments, if one investment drops in value, others could potentially offset losses and stabilize your portfolio’s value.

Consider investing in mutual funds and ETFs (exchange-traded funds), which offer built-in diversification through professionally managed baskets of securities. Mutual funds are priced at the end of the trading day based on their net asset value (NAV), while ETFs trade throughout the day at market prices. If you’re new to investing, ETFs may be preferable due to their lower account minimums.

Monitor your allocation regularly and revisit your recurring investment plan annually to ensure you remain on track to reach your goals. If you receive pay raises, consider increasing your savings amounts accordingly. This ongoing attention to asset allocation, combined with consistent automatic contributions, creates a powerful foundation for building retirement wealth from zero savings.

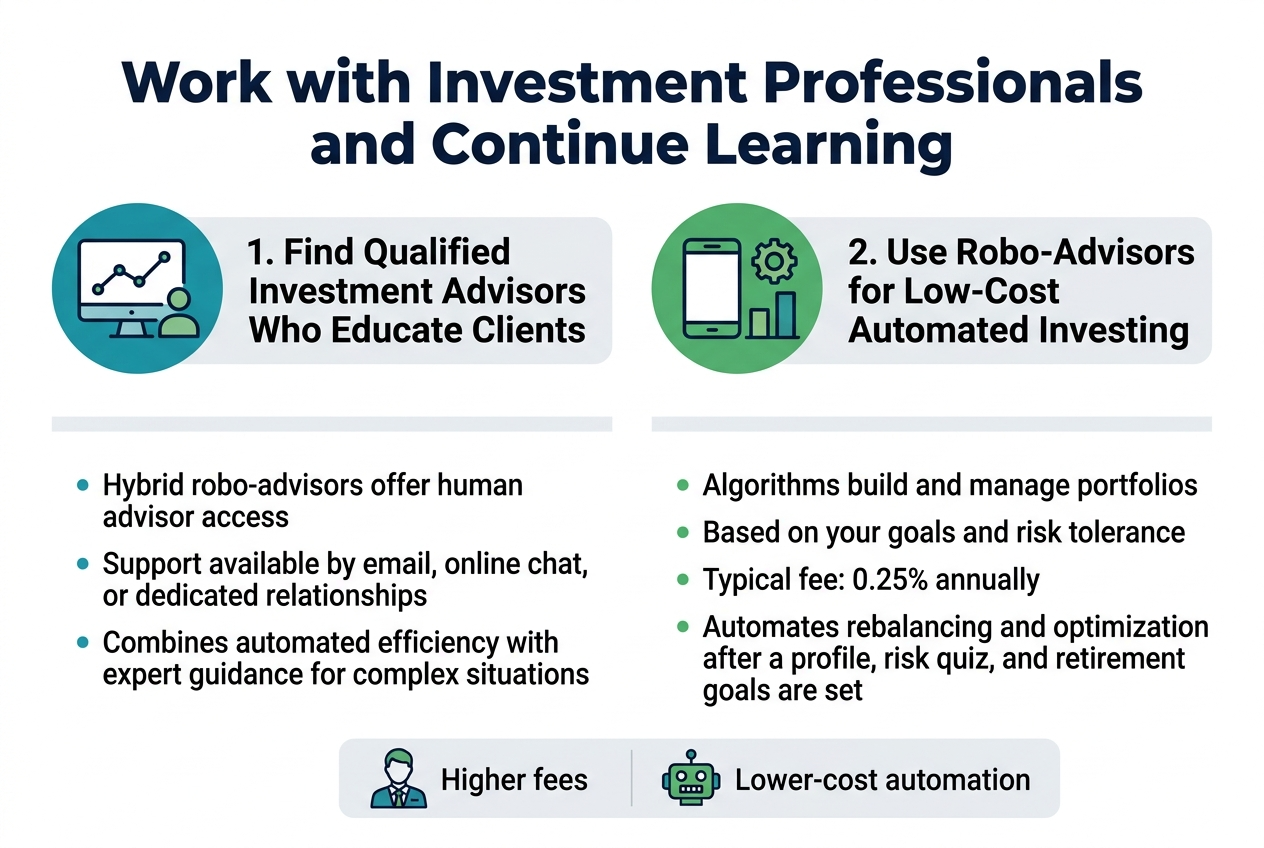

Work with Investment Professionals and Continue Learning

Find Qualified Investment Advisors Who Educate Clients

With your foundation established, working with qualified investment professionals becomes crucial for long-term success. Many robo-advisors now offer access to human financial advisors through email, online chat, or dedicated advisor relationships, providing personalized guidance beyond automated portfolio management. These hybrid services combine computer-driven efficiency with human expertise for complex financial situations.

Use Robo-Advisors for Low-Cost Automated Investing

Robo-advisors automate investment management using computer algorithms to build and manage portfolios based on your goals and risk tolerance. They charge significantly lower fees than traditional financial advisors – typically around 0.25% annually compared to much higher human advisor fees. The enrollment process involves creating a financial profile, taking a risk attitude quiz, and setting retirement goals, after which smart technology handles rebalancing and optimization automatically.

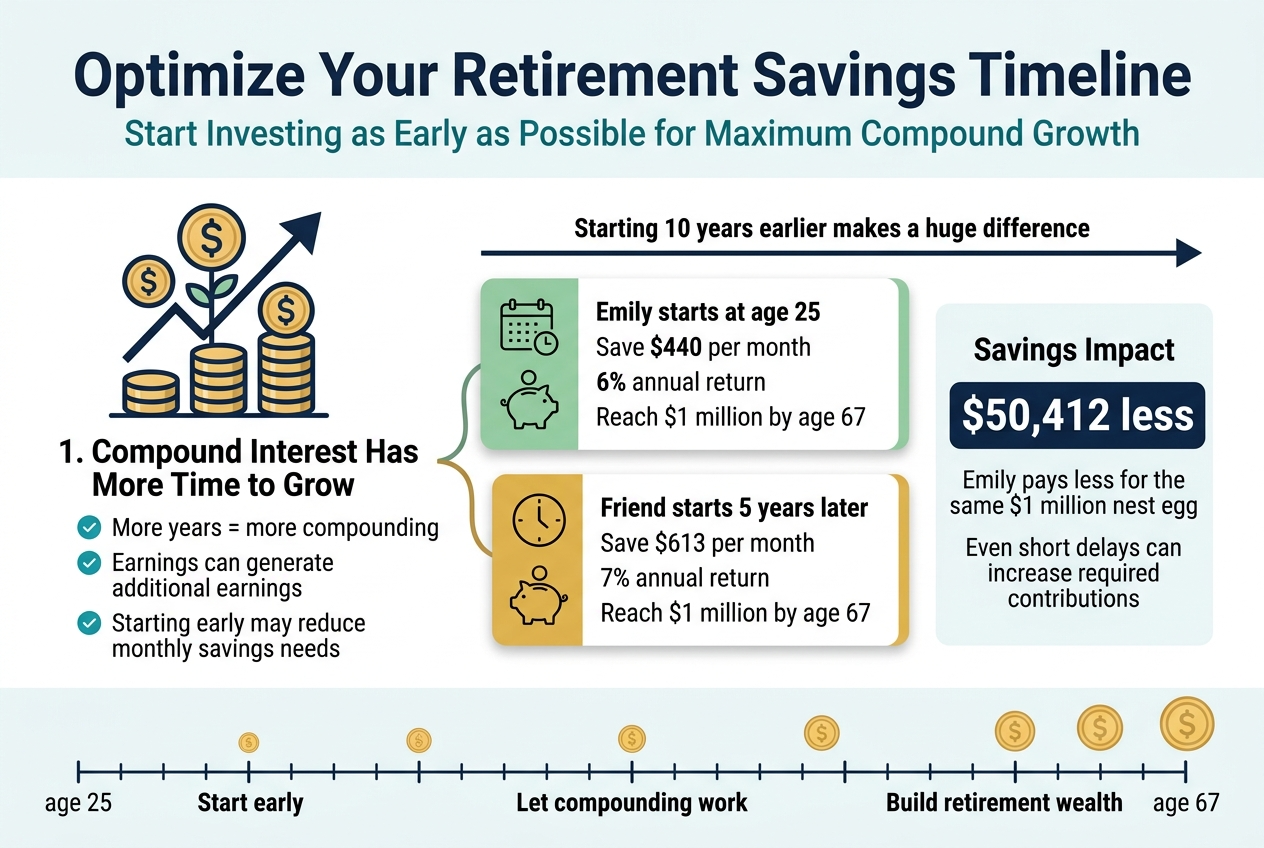

Optimize Your Retirement Savings Timeline

Start Investing as Early as Possible for Maximum Compound Growth

Now that we have covered the essential steps for building your retirement investment strategy, timing becomes your most powerful ally. Compound interest gives your retirement savings a significant boost, as the more time your money has to compound and grow, the more opportunity for those earnings to earn additional money. Starting early means you may not have to set aside as much money as you would if you began investing later.

Understand the Million-Dollar Impact of Starting 10 Years Earlier

Previously, I’ve shown you how to select investments and implement your strategy, but the timeline makes an extraordinary difference in your results. A hypothetical example demonstrates this power: Emily, starting at age 25, only needs to save $440 monthly to reach $1 million by age 67, assuming a 6% annual return. Her friend who waits just five years must contribute $613 monthly at 7% returns to achieve the same goal. Emily ultimately pays $50,412 less for her million-dollar nest egg, proving that even short delays can cost tens of thousands in additional contributions required.

Building retirement wealth from zero savings may seem daunting, but with the right strategy and commitment, anyone can secure their financial future. The key is following a proven step-by-step approach: establish your financial foundation by eliminating debt and building an emergency fund, set clear investment goals, choose tax-advantaged accounts like 401(k)s and Roth IRAs, and consistently invest 15% of your income in diversified mutual funds. Remember that time is your greatest asset—the sooner you start, the more compound growth can work in your favor.

The path to retirement wealth isn’t about timing the market or finding the perfect investment—it’s about developing consistent habits and staying disciplined over the long term. Whether you’re 25 or 55, the principles remain the same: live debt-free, invest regularly, diversify your portfolio, and work with investment professionals who can guide you along the way. Take action today by evaluating your current financial situation and taking the first step toward building the retirement you deserve. Your future self will thank you for the decisions you make right now.