Are you tired of watching your hard-earned money sit IDLE in savings accounts, earning barely enough to buy a cup of coffee each month? Do you find yourself scrolling through investment apps, feeling overwhelmed by countless options that promise the moon but might leave you broke? You’re not alone in this financial maze. Millions of Indians today are searching for investment opportunities that offer the perfect balance between GROWTH & security.

In today’s volatile economic climate, finding safe investment options has become more crucial than ever before. While the stock market might give you heart palpitations with its daily ups & downs, there are several time-tested investment vehicles that can help you build wealth steadily without losing sleep. Think of these investments as the tortoise in the famous race against the hare they might not sprint ahead dramatically, but they consistently move forward toward the FINISH line.

This comprehensive guide will walk you through five proven investment options that have stood the test of time in India’s financial landscape. We’ll explore everything from government backed schemes to traditional investment methods that your grandparents probably swore by. Each option we discuss offers a unique combination of safety, liquidity, & reasonable returns that can help you achieve your financial goals without unnecessary stress. Whether you’re a CAUTIOUS first-time investor or someone looking to diversify their portfolio with stable options, these investments deserve serious consideration in your wealth-building journey.

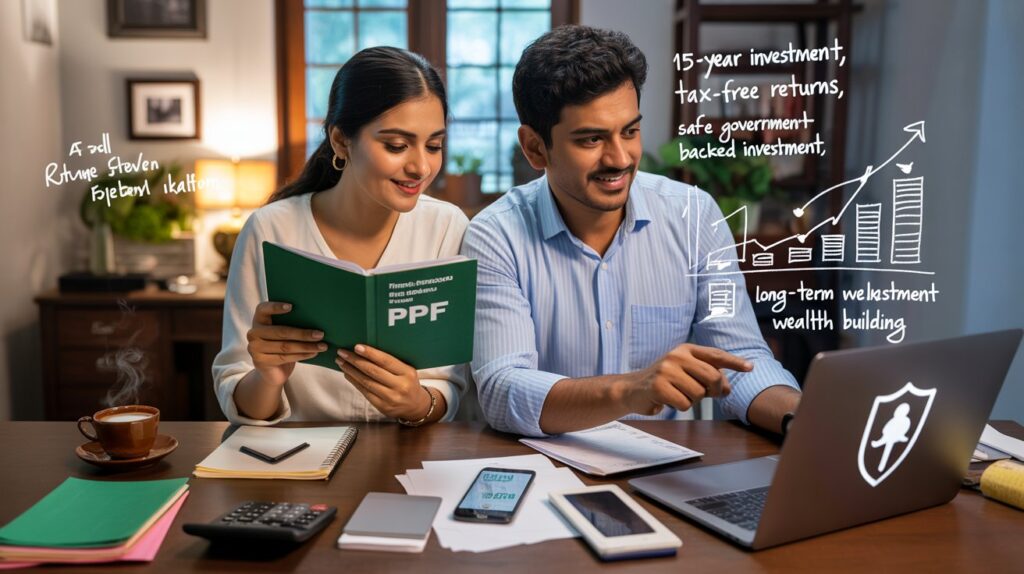

1. Public Provident Fund (PPF) – The GOLD Standard of Safe Investments

Have you ever wondered why financial advisors across India consistently recommend PPF as a cornerstone investment? The Public Provident Fund isn’t just another investment scheme – it’s like having a PROTECTIVE financial umbrella that shields your money from taxes while helping it grow steadily over fifteen years. Currently offering an attractive interest rate of 7.1% annually, PPF stands out as one of the most reliable long-term investment options available to Indian citizens.

The beauty of PPF lies in its triple benefit structure that makes it incredibly appealing to SMART investors. First, every rupee you invest in PPF qualifies for tax deduction under Section 80C, reducing your taxable income by up to ₹1.5 lakhs annually. Second, the interest earned on your PPF account remains completely tax-free, meaning more money stays in your pocket instead of going to the government. Third, the maturity amount after fifteen years is entirely tax-exempt, creating a powerful wealth-building tool that COMPOUNDS your returns effectively.

What makes PPF particularly attractive is its government backing, which essentially eliminates any risk of losing your principal amount. Unlike market-linked investments that can fluctuate wildly, your PPF account grows steadily each year, making it perfect for risk-averse investors who prioritize capital PRESERVATION over aggressive growth. The minimum annual investment requirement of just ₹500 makes it accessible to virtually everyone, while the maximum limit of ₹1.5 lakhs ensures that even high-income individuals can benefit significantly from this scheme.

Consider this real example if you invest the maximum ₹1.5 lakhs annually in PPF for fifteen years at the current interest rate, you’ll contribute ₹22.5 lakhs in total but receive approximately ₹43 lakhs at MATURITY. This nearly doubles your investment through the magic of compound interest, all while enjoying complete tax benefits throughout the investment period.

2. National Savings Certificate (NSC) – The TRADITIONAL Powerhouse

Why do millions of Indians continue to trust National Savings Certificates despite the emergence of countless modern investment options? NSC represents the perfect blend of traditional RELIABILITY & contemporary returns, offering investors a government-guaranteed way to grow their wealth over five years. With current interest rates hovering around 6.8% annually, NSC provides predictable returns that help investors plan their financial future with confidence.

The SIMPLICITY of NSC is perhaps its greatest strength, making it ideal for investors who prefer straightforward investment mechanisms without complex terms & conditions. You can purchase NSC from any post office across India, making it incredibly accessible even in remote areas where sophisticated financial services might not be available. The investment process is refreshingly UNCOMPLICATED – simply walk into a post office, fill out a form, pay your money, & receive a certificate that guarantees your returns.

NSC offers significant tax advantages that make it particularly attractive during tax-planning season. Your investment qualifies for deduction under Section 80C, while the ACCRUED interest is reinvested automatically, creating a compounding effect that maximizes your returns. Although you’ll need to pay tax on the interest upon maturity, the overall tax efficiency makes NSC a valuable addition to any conservative investor’s PORTFOLIO.

One interesting feature of NSC is its ability to serve as collateral for loans from banks, providing LIQUIDITY options even though the investment itself has a fixed five-year lock-in period. This flexibility can prove invaluable during financial emergencies when you need access to funds but don’t want to break your investment. Additionally, NSC can be transferred from one person to another, making it useful for ESTATE planning & family financial management.

3. Fixed Deposits (FDs) – The RELIABLE Old Friend

What investment option comes to mind when you think about absolute safety & guaranteed returns in India? Fixed Deposits have been the go-to choice for CONSERVATIVE investors for decades, offering predictable returns ranging from 3% to 7% depending on the bank, tenure, & deposit amount. While FD rates might seem modest compared to equity markets during BULL runs, they provide unmatched peace of mind & capital protection that many investors value above aggressive growth potential.

The FLEXIBILITY that Fixed Deposits offer is truly remarkable, catering to diverse financial needs & investment horizons. You can choose tenure periods ranging from seven days to ten years, allowing you to align your investments with specific financial goals. Short-term FDs work perfectly for EMERGENCY funds or money you’ll need within a year, while longer-term deposits can serve as conservative components of your retirement planning strategy. Many banks also offer auto-renewal features, ensuring your money continues earning returns even if you FORGET to reinvest manually.

Modern banking has revolutionized the FD experience, making it possible to open deposits online within minutes using mobile apps or internet banking platforms. This CONVENIENCE factor has made FDs even more appealing to busy professionals who want to invest quickly without visiting bank branches. Additionally, senior citizens often enjoy preferential interest rates on Fixed Deposits, typically earning an additional 0.25% to 0.5% above regular rates.

However, it’s important to understand that FD interest is fully TAXABLE according to your income tax slab, which can impact your net returns. Many investors use FD laddering strategies, where they create multiple Fixed Deposits with different maturity dates to ensure regular LIQUIDITY while maximizing returns. This approach helps manage interest rate risks & provides flexibility to reinvest at potentially better rates when deposits mature.

4. Government Bonds & Treasury Bills – The SOVEREIGN Safety Net

Have you ever considered lending money to the government & earning steady returns for your generosity? Government bonds & Treasury Bills represent one of the SAFEST investment categories available anywhere in the world, as they carry the full faith & backing of the Indian government. These instruments offer returns ranging from 6% to 8% annually, depending on the tenure & prevailing interest rate environment.

Treasury Bills, commonly known as T-Bills, are SHORT-TERM government securities with maturities of 91 days, 182 days, & 364 days. They’re sold at a discount to their face value & redeemed at full value upon maturity, with the difference representing your PROFIT. For instance, a ₹100 T-Bill might be available for ₹97, giving you a ₹3 return when it matures. While this might seem small, the annualized returns can be quite attractive, especially for parking SURPLUS funds for short periods.

Government bonds, on the other hand, offer longer TENURE options ranging from five to forty years, making them suitable for long-term wealth building & retirement planning. These bonds pay regular interest, typically semi-annually, providing a steady INCOME stream that many investors find appealing. Recent government initiatives have made these bonds accessible to retail investors through various platforms, democratizing access to instruments that were previously available mainly to institutional INVESTORS.

One significant advantage of government securities is their LIQUIDITY in secondary markets, allowing you to sell before maturity if needed. This feature provides flexibility that traditional instruments like PPF & NSC don’t offer. Additionally, certain government bonds offer inflation-indexed returns, protecting your PURCHASING power against rising prices over time.

5. Senior Citizen Savings Scheme (SCSS) & Sukanya Samriddhi Yojana – SPECIALIZED Safety Options

Why should age & family status influence your investment choices? India’s financial ecosystem includes several SPECIALIZED schemes designed for specific demographics, offering enhanced returns & benefits tailored to unique needs. The Senior Citizen Savings Scheme provides attractive returns of around 8% annually for investors aged 60 & above, recognizing their need for stable INCOME during retirement years.

SCSS stands out for its quarterly interest payments, providing regular CASH flow that many retirees find essential for managing monthly expenses. The scheme allows investments up to ₹15 lakhs with a five-year tenure that can be extended for an additional three years. This FLEXIBILITY makes SCSS perfect for retirees who want guaranteed income without the volatility of market-linked investments.

Sukanya Samriddhi Yojana represents another BRILLIANT specialized option designed specifically for girl children, currently offering returns of around 7.6% annually. This scheme combines the benefits of long-term wealth creation with substantial tax advantages, making it an excellent tool for securing your daughter’s FUTURE education & marriage expenses. The 21-year tenure might seem long, but the tax-free maturity proceeds & compound growth make it incredibly powerful for building substantial WEALTH.

What makes these specialized schemes particularly attractive is their ENHANCED returns compared to general investment options. The government deliberately offers better rates to encourage specific financial behaviors – retirement planning for seniors & girl child welfare through Sukanya Samriddhi Yojana. Both schemes enjoy complete government BACKING, ensuring absolute safety of your principal investment.

Building Your Financial FORTRESS: Key Takeaways & Action Steps

Your journey toward financial security doesn’t require complicated strategies or HIGH-RISK gambles that keep you checking stock prices every hour. The five investment options we’ve explored represent time-tested paths to building wealth steadily while preserving your hard-earned capital. Each offers unique advantages that can fit seamlessly into your overall financial PLAN, whether you’re just starting your investment journey or looking to add stable components to an existing portfolio.

Remember that successful investing isn’t about finding the single PERFECT investment but rather creating a balanced approach that aligns with your risk tolerance, financial goals, & life circumstances. Consider combining several of these SAFE options to create a diversified foundation for your wealth. For instance, you might use PPF for long-term tax-free growth, maintain some money in Fixed Deposits for EMERGENCY access, & invest in government bonds for regular income.

The BEAUTY of these conservative investments lies not just in their safety but in their ability to provide peace of mind that allows you to focus on other important aspects of life. While aggressive investments might offer higher returns, they often come with stress & uncertainty that can impact your overall QUALITY of life. These stable options ensure steady progress toward your financial goals without the emotional rollercoaster of volatile markets.

Take ACTION today by evaluating which of these options align best with your current financial situation & future goals. Start small if necessary, but start NOW – time & consistent investing are your greatest allies in building long-term wealth. Your future self will thank you for choosing the steady, reliable path to financial INDEPENDENCE over risky shortcuts that might lead nowhere.