Picture this: You’re DILIGENTLY putting away ₹5,000 every month into your savings account, feeling PROUD of your financial discipline. But somehow, your bank balance isn’t growing as fast as you expected. You’re scratching your head, wondering where all your HARD-EARNED money is disappearing. Sound familiar? You’re not alone in this frustrating journey.

Millions of Indians are facing this EXACT same problem right now. They think they’re being smart with their money, but there are HIDDEN villains quietly eating away at their savings. These aren’t the obvious expenses like rent or groceries that you can easily spot. Instead, they’re the sneaky, almost INVISIBLE costs that creep into your life without making much noise.

The year 2026 has brought NEW challenges for Indian savers. With RISING inflation, changing digital payment habits, & evolving lifestyle patterns, these hidden expenses have become even MORE dangerous. They’re like termites in your house – you don’t see them, but they’re slowly destroying the FOUNDATION of your financial future.

Think about it: What if I told you that you might be losing THOUSANDS of rupees every month without even realizing it? What if these small, seemingly harmless expenses are the REAL reason you can’t afford that dream vacation or can’t build an emergency fund? This article will EXPOSE seven major culprits that are silently draining your savings account. More importantly, you’ll learn PRACTICAL ways to fight back & protect your money.

1. The ATM Fee TRAP That’s Costing You More Than You Think

Have you ever needed cash urgently & just grabbed money from the NEAREST ATM without thinking twice? Most Indians do this regularly, but here’s the SHOCKING truth: those small ATM fees are adding up to MASSIVE amounts over time.

Banks in India typically charge ₹20-25 for using other bank ATMs after your FREE transaction limit. This might seem tiny, but let’s do some SIMPLE math. If you use other bank ATMs just twice a week, you’re paying around ₹200 per month. That’s ₹2,400 per year! For a family of four, this could easily become ₹10,000 annually.

But wait, there’s MORE to this story. In 2026, many banks have also started charging for SMS alerts, mini-statements, & even balance inquiries at ATMs. These “convenience charges” might be just ₹2-5 each time, but they’re like DEATH by a thousand cuts. Sarah, a working professional from Bangalore, discovered she was paying ₹150 monthly just in various ATM fees. When she calculated her yearly loss, she was SHOCKED to find it was enough to buy a new smartphone.

The solution is SURPRISINGLY simple. Plan your cash withdrawals from your own bank’s ATMs. Use digital payments whenever possible. Keep track of your FREE transaction limits & make larger withdrawals less frequently instead of small ones regularly. Your future self will THANK you for these small changes.

2. Subscription Services: The MONTHLY Vampires Sucking Your Account Dry

Remember when you signed up for that Netflix subscription for a SPECIAL weekend binge? Or when you downloaded that fitness app with a “just ₹99 for the first month” offer? These subscription services are MASTERS of disguise, appearing helpful while quietly draining your savings every single month.

The AVERAGE Indian urban household now has 6-8 active subscriptions running simultaneously. Netflix, Amazon Prime, Spotify, various gaming apps, cloud storage, fitness apps, food delivery passes, & magazine subscriptions. Each one seems AFFORDABLE individually, but together they create a monthly monster that can easily cross ₹2,000-3,000.

Here’s what makes this problem WORSE in 2026: Many apps now use dynamic pricing & auto-renewal tricks. They might offer you a GREAT introductory price, then quietly increase it after a few months. Rajesh from Mumbai recently discovered his music streaming app had increased from ₹99 to ₹179 per month without any clear notification. He had been paying the higher amount for EIGHT months without realizing it.

The SNEAKY part about subscriptions is how they make you feel guilty for canceling. “You’ll lose all your playlists!” or “Your saved data will be deleted!” they warn. But ask yourself honestly: How many of these services do you ACTUALLY use regularly? Conduct a monthly audit of your subscriptions. Cancel the ones you haven’t used in the past 30 days. For the ones you keep, set calendar REMINDERS to review them every three months.

3. Credit Card Interest: The INVISIBLE Monster Growing in Your Wallet

Credit cards can be FANTASTIC financial tools when used wisely, but they can also become your worst nightmare without proper management. The MOST dangerous part isn’t the obvious interest on unpaid balances – it’s all the HIDDEN costs that come with poor credit card habits.

Many Indians fall into the “minimum payment” trap. Banks LOVE to highlight how you only need to pay a small percentage of your total bill. What they don’t emphasize is that the remaining amount attracts interest rates of 36-48% annually. If you have a ₹50,000 balance & only pay the minimum amount, you could end up paying over ₹15,000 in interest alone over the next year.

But there are SNEAKIER costs too. Late payment fees (usually ₹500-1,500), over-limit charges, cash advance fees, & foreign transaction charges. Priya from Chennai thought she was being SMART by using her credit card for everything to earn reward points. However, she occasionally missed payment dates due to her BUSY schedule. The late fees & interest charges completely wiped out any benefits from her reward points, plus cost her an additional ₹8,000 annually.

Cash advances are another HIDDEN trap. Taking cash from your credit card might seem convenient, but banks charge both a percentage fee (2-3%) plus immediate interest from day one. There’s no grace period like regular purchases. The SMART approach is treating your credit card like a debit card – only spend what you can pay back IMMEDIATELY. Set up automatic payments for the full amount, not just the minimum.

4. Digital Payment Convenience Charges: The MODERN Day Highway Robbery

The digital revolution in India has made payments INCREDIBLY convenient, but it has also created new opportunities for companies to charge small fees that add up SIGNIFICANTLY over time. These convenience charges are the NEW-AGE pickpockets of the financial world.

Every time you pay your electricity bill online, book movie tickets, recharge your phone, or pay for services through apps, there’s often a small “convenience fee” or “processing charge” added. These typically range from ₹5-50 per transaction. For someone who pays 10-15 bills monthly through digital platforms, this could easily add up to ₹500-800 per month, or nearly ₹10,000 per year.

The TRICKY part is how these charges are presented. They’re usually shown at the final payment step, when you’re already committed to the transaction. Many people just click “proceed” without carefully reading the BREAKDOWN. Amit, a software engineer from Hyderabad, decided to track these charges for three months. He was AMAZED to discover he was paying ₹1,200 monthly just in various convenience fees.

Food delivery apps are PARTICULARLY notorious for this practice. They might show a dish for ₹200, but by the time you check out, there’s delivery fee, platform fee, GST, & sometimes even a “small order fee.” A ₹200 meal can easily become ₹300-350 with all these additions. The SMART strategy is always checking if direct payment options are available (like paying directly on restaurant websites) & comparing total costs, not just base prices.

5. Insurance OVER-Coverage: When Protection Becomes Financial Destruction

Insurance is ABSOLUTELY necessary for financial security, but many Indians are paying for WAY more coverage than they actually need, or worse, paying for the WRONG types of insurance altogether. This over-insurance problem has become a MAJOR hidden expense in 2026.

The BIGGEST culprit is often Life Insurance policies that combine investment & insurance. These products typically offer poor returns on the investment portion while charging HIGH fees. Many families end up paying ₹50,000-1,00,000 annually for policies that could be replaced with ₹10,000 term insurance plus separate investments with BETTER returns.

Multiple health insurance policies are another COMMON mistake. Having insurance from your employer, plus a family floater, plus individual policies for each family member creates UNNECESSARY overlap. You can’t claim the same medical expense from multiple insurers, so you’re essentially paying multiple premiums for single coverage.

Vehicle insurance is another area where people OVERSPEND without realizing it. Many car owners automatically renew comprehensive insurance every year without comparing prices or adjusting coverage. Rohit from Delhi discovered he could save ₹8,000 annually just by comparing insurance providers & adjusting his car’s Insured Declared Value to its CURRENT market price instead of the original purchase price.

The GOLDEN rule for insurance is: insure what you cannot afford to lose, & self-insure what you can. Review all your insurance policies annually. Make sure you’re not paying for DUPLICATE coverage & that your coverage amounts match your actual current needs, not your needs from five years ago.

6. Impulse Shopping: The EMOTIONAL Spending That’s Bankrupting Your Future

Impulse shopping has become DANGEROUSLY easy in 2026, thanks to one-click payments, instant delivery, & AI-powered recommendation systems that know exactly what you want before you do. This isn’t just about buying unnecessary items – it’s about how modern technology has made EMOTIONAL spending almost inevitable.

The AVERAGE Indian smartphone user receives 15-20 shopping notifications daily. Flash sales, limited-time offers, “last piece” warnings, & personalized discounts create artificial urgency that triggers impulsive decisions. E-commerce platforms have become MASTERS at psychological manipulation, using techniques like showing “5 people are viewing this item” or “Only 2 left in stock” to create panic buying.

Social media has made this problem EXPONENTIALLY worse. Instagram & Facebook ads are no longer obvious advertisements – they’re carefully crafted content that feels like recommendations from friends. Influencer marketing has made impulse shopping feel like lifestyle choices rather than financial decisions. Kavya, a marketing professional from Pune, realized she was spending ₹15,000 monthly on items she saw on social media but barely used.

Buy-now-pay-later services have removed the IMMEDIATE pain of spending, making impulse purchases feel almost free. When you can buy a ₹10,000 gadget for just ₹2,500 today & pay the rest later, your brain doesn’t register the FULL financial impact. However, juggling multiple such payments can quickly spiral out of control.

The MOST effective defense against impulse shopping is the 24-hour rule for any purchase over ₹1,000. Add items to your cart, but wait a full day before buying. You’ll be SURPRISED how many items suddenly seem unnecessary after a good night’s sleep.

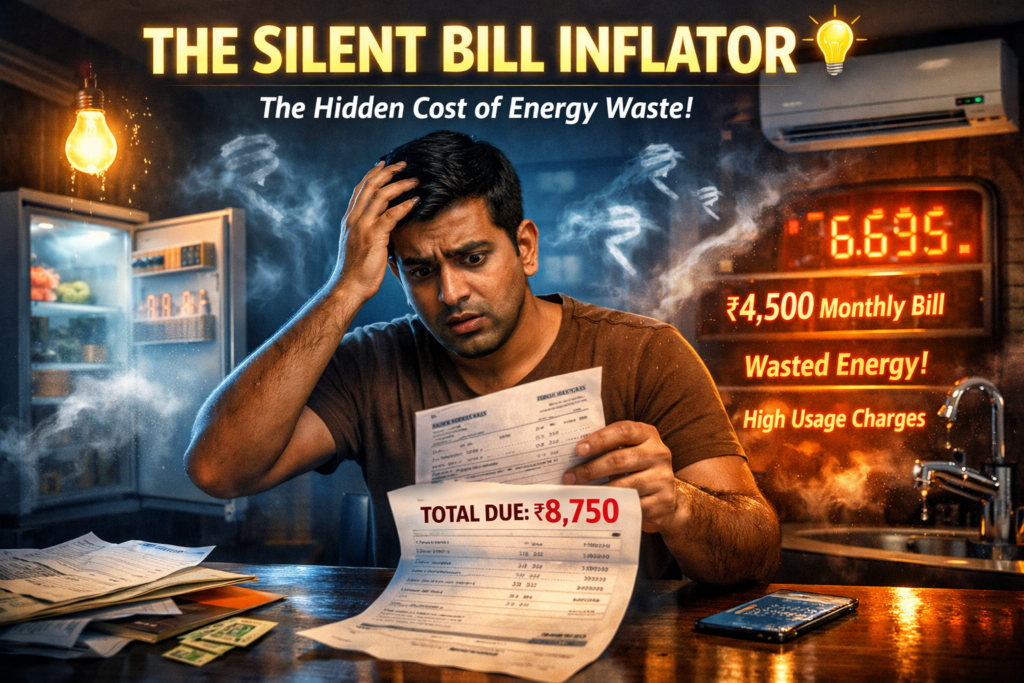

7. Energy & Utility Waste: The SILENT Bill Inflator Nobody Talks About

Your electricity, gas, & water bills might seem like fixed expenses, but INEFFICIENT usage & poor habits are adding unnecessary costs that compound month after month. In 2026, with RISING energy costs across India, these wasteful practices have become even more expensive.

Old appliances are often the BIGGEST culprits. A 10-year-old air conditioner can consume 40-50% more electricity than a new 5-star rated model. Similarly, old refrigerators, washing machines, & water heaters can be SILENTLY inflating your monthly bills. The cost difference might seem small monthly, but over a year, it can easily reach ₹15,000-25,000 for a typical household.

Standby power consumption is another HIDDEN expense. Electronics like televisions, set-top boxes, computers, & phone chargers continue consuming electricity even when not in use. This “phantom load” can account for 5-10% of your total electricity bill. For a family with a monthly bill of ₹3,000, that’s ₹300-600 monthly, or ₹7,200 annually, just for powering devices that aren’t even being used.

Water heating habits are PARTICULARLY expensive. Many families keep their geyser running throughout winter days, even when nobody’s home. Running a 15-litre geyser for 8 hours daily can add ₹1,500-2,000 to your monthly electricity bill. Smart scheduling & using geysers only when needed can cut this cost by 60-70%.

Simple changes like switching to LED bulbs, using smart power strips, timing your geyser usage, & maintaining appliances properly can DRAMATICALLY reduce these hidden costs. Regular servicing of air conditioners & refrigerators not only extends their life but also improves their EFFICIENCY significantly.

Take CONTROL of Your Financial Future Today

Now that you’ve discovered these SEVEN hidden money drains, you might be feeling overwhelmed or even frustrated about how much you’ve been unknowingly spending. That’s completely NORMAL & actually a good sign – it means you’re ready to take action & make positive changes.

The MOST important thing to remember is that small changes create big results over time. You don’t need to tackle all these problems at once. Start with the area that’s costing you the MOST money, or the one that seems easiest to fix. Even addressing just two or three of these hidden expenses could save you ₹20,000-50,000 annually.

Create a monthly “expense audit” routine. Spend 30 minutes each month reviewing your bank statements, credit card bills, & subscription services. Look for charges you don’t recognize or services you’re not using. This simple habit alone can save THOUSANDS of rupees every year.

Remember, the goal isn’t to live like a miser or deprive yourself of everything enjoyable. It’s about making CONSCIOUS decisions about where your money goes instead of letting it slip away unnoticed. When you plug these hidden leaks, you’ll have MORE money available for the things that truly matter to you – whether that’s a family vacation, a new home, or a comfortable retirement.

Your FUTURE self is depending on the financial decisions you make today. Every rupee you save from these hidden expenses is a rupee that can grow through proper investments & compound over time. Start today, start small, but most importantly, just START. Your journey toward better financial health begins with awareness, & now you have the knowledge to make it happen.